What is the difference between Form 16 and Form 16A? is a common question among Indian taxpayers, especially during the income tax filing season. Both forms serve as TDS certificates issued by different entities for different types of income, yet many people confuse them or use the terms interchangeably. Understanding the distinction between these two important documents helps you file your income tax returns accurately and claim the correct tax credits, preventing unnecessary complications with tax authorities.

What is the Difference Between Form 16 and Form 16A?

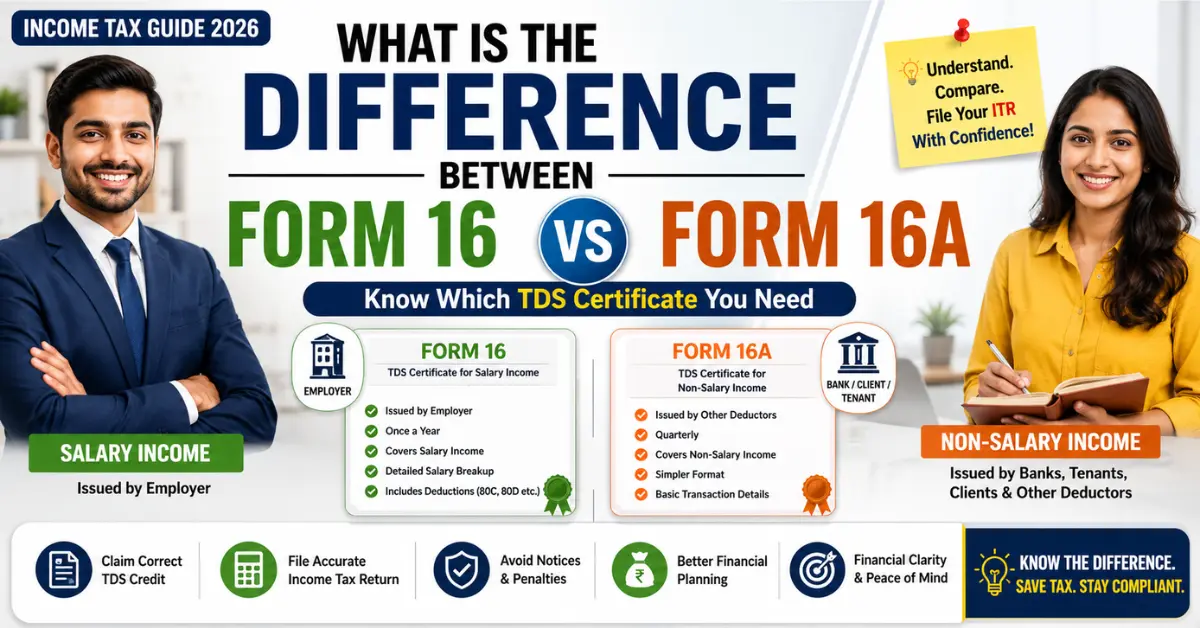

Form 16 and Form 16A are both Tax Deducted at Source certificates issued in India, but they differ fundamentally in who issues them and what type of income they cover. Form 16 is issued by employers to salaried employees for tax deducted from salary income, while Form 16A is issued by any other deductor for tax deducted from non-salary payments.

The primary distinction lies in the nature of income and the relationship between the deductor and deductee. Therefore, understanding which form applies to your situation depends entirely on how you earned the income and who deducted tax from it.

Moreover, both forms play crucial roles during income tax return filing, serving as proof that tax has already been deducted and deposited with the government on your behalf. This prevents double taxation and ensures you receive credit for taxes already paid.

What is Form 16?

Form 16 meaning refers to a certificate issued by employers to their salaried employees showing the total salary paid and tax deducted during a financial year. This document is mandatory for all employers who deduct tax at source from employee salaries.

The Income Tax Department mandates that employers issue Form 16 by June 15th each year for the previous financial year. For example, Form 16 for the financial year 2023-24 should be issued by June 15, 2024.

Form 16 contains two parts providing comprehensive salary and tax information. Part A includes basic details like employer and employee information, TAN and PAN numbers, summary of tax deducted and deposited quarterly, and acknowledgement numbers of quarterly TDS returns filed by the employer.

Part B provides a detailed breakdown of your salary structure including basic pay, allowances, perquisites, deductions claimed under various sections like 80C, 80D, and the final taxable income. This section helps employees verify that their employer calculated tax correctly based on declared investments and expenses.

Additionally, Form 16 serves as an essential document when applying for loans, visas, or any financial verification where income proof is required. Banks and financial institutions widely accept it as valid income documentation.

For salaried individuals, Form 16 simplifies tax filing considerably. Most details required for ITR filing are readily available in this single document, reducing chances of errors and making the process faster.

What is Form 16A?

Form 16A meaning applies to TDS certificates issued for income other than salary. This form is issued by anyone who deducts tax at source from payments made to you, excluding employers paying salaries.

Common scenarios where Form 16A gets issued include interest income from fixed deposits where banks deduct TDS, rent payments where tenants deduct TDS, professional fees where clients deduct TDS, commission income where companies deduct TDS, and contract payments where contractors face TDS deduction.

For instance, if you are a freelance graphic designer and your client deducts TDS from your invoice payment, they must issue Form 16A. Similarly, if you rent out property and your tenant deducts TDS on rent exceeding Rs. 50,000 monthly, they should provide Form 16A.

Form 16A contains details like the deductor's name, address, TAN, and PAN, your PAN as the deductee, the nature of payment, gross amount paid, tax deducted, and the date of tax deposit with the government.

Unlike Form 16 which is issued once annually, Form 16A is issued quarterly. Each quarter's certificate covers transactions and TDS deductions for that specific three-month period, requiring careful tracking if you receive multiple Form 16As from different sources.

Freelancers, consultants, property owners, and anyone earning non-salary income must collect Form 16A from all parties who deducted TDS. These certificates become crucial evidence while filing income tax returns and claiming TDS credit.

Key Differences Between Form 16 and Form 16A Explained

Understanding the difference between Form 16 and 16A requires examining several aspects where these documents diverge significantly.

Type of Income Covered: Form 16 exclusively covers salary income including all components like basic pay, allowances, bonuses, and perquisites. In contrast, Form 16A covers all other incomes such as interest, rent, professional fees, commission, and contract payments.

Who Issues the Certificate: Only employers issue Form 16 to their salaried employees. However, Form 16A can be issued by banks, tenants, clients, companies, or any entity that deducts TDS on non-salary payments.

Frequency of Issuance: Form 16 is issued once a year after the financial year ends, typically by June 15th. Form 16A is issued quarterly, meaning you might receive up to four certificates per year from the same deductor.

Format and Structure: Form 16 has two parts with Part B containing detailed salary breakup and deductions claimed. Form 16A has a simpler single-part format focusing primarily on transaction details and TDS deducted.

Information Provided: Form 16 includes comprehensive salary structure, exemptions claimed, deductions under Chapter VI-A like 80C, 80D, and net taxable income. Form 16A provides basic transaction information, amount paid, and TDS deducted without detailed breakup.

Legal Provisions: Form 16 falls under Section 203 of the Income Tax Act and relates to salary TDS covered under Section 192. Form 16A also falls under Section 203 but relates to other TDS sections like 194A for interest, 194I for rent, 194J for professional fees, and others.

Who Receives Form 16 and Who Receives Form 16A?

Knowing whether you should receive Form 16, Form 16A, or both depends entirely on your income sources and employment status.

Who Receives Form 16: All salaried employees whose employers deduct TDS from their salaries receive Form 16. This includes full-time employees, part-time salaried staff, contract employees on the payroll, and anyone receiving regular salary with TDS deduction.

Even if your total income falls below the taxable limit but your employer deducted TDS, you are entitled to receive Form 16. This certificate helps you claim a refund of excess tax deducted when filing your return.

Who Receives Form 16A: Individuals earning non-salary income where TDS is applicable receive Form 16A. This includes freelancers and consultants receiving professional fees, property owners receiving rent above threshold limits, fixed deposit holders from whose interest banks deduct TDS, commission agents, contractors, and anyone receiving payments subject to TDS provisions.

Many people receive both forms if they have salary income plus additional income sources. For example, a salaried employee who also earns rental income would receive Form 16 from their employer and Form 16A from their tenant if TDS is deducted.

Therefore, track all your income sources and ensure you receive appropriate TDS certificates from each deductor. Missing certificates can complicate tax filing and delay refunds.

Why These Forms Matter While Filing ITR in India

TDS certificate India documents like Form 16 and Form 16A serve critical functions during income tax return filing, making them indispensable for accurate tax compliance.

Firstly, these forms provide ready information about your income and taxes already paid. This data directly feeds into your ITR, reducing manual calculations and potential errors in reporting.

Moreover, Form 16 and Form 16A serve as proof that tax has been deducted and deposited with the government on your behalf. When you file your return, you claim credit for this TDS, which gets adjusted against your total tax liability.

The Income Tax Department matches TDS claimed in your return with the data from these certificates. Any mismatch triggers notices and demands for clarification, potentially delaying refunds or causing assessment issues.

Additionally, if tax deducted exceeds your actual tax liability, these certificates help you claim refunds. Without proper documentation, proving excess tax payment becomes difficult, and you might lose money rightfully yours.

For audit purposes, maintaining these certificates for at least six years as per Income Tax Act provisions protects you during scrutiny or reassessment proceedings. They provide concrete evidence supporting your tax filings.

Furthermore, these forms contain your deductor's details including their TAN. This information helps tax authorities track whether deductors deposited the TDS they deducted, ensuring compliance throughout the tax chain.

Common Misconceptions Taxpayers Have

Several misunderstandings about Form 16 and Form 16A create confusion among Indian taxpayers, leading to errors or missed opportunities.

Misconception 1: Form 16 is Mandatory Only If Tax is Payable

Many believe employers need not issue Form 16 if total income is below taxable limits. This is incorrect. If an employer deducted TDS at any point during the year, they must issue Form 16 regardless of final tax liability.

Misconception 2: Form 16A Can Replace Form 16

Some think receiving Form 16A from an employer for non-salary payments substitutes for Form 16. However, for salary income, specifically Form 16 must be issued. Form 16A applies only to non-salary transactions.

Misconception 3: You Can File ITR Without These Forms

While technically possible to file returns without these certificates, doing so is highly inadvisable. You risk claiming incorrect TDS, facing mismatches, and inviting tax department scrutiny.

Misconception 4: Digital Access Makes Physical Certificates Unnecessary

Although TDS details are available on the TRACES portal and Form 26AS, having actual certificates from deductors remains important. They provide additional details and serve as first-hand documentation from the deductor.

Misconception 5: Late Issuance Means Invalid Certificates

Some worry that certificates issued after due dates become invalid. While deductors face penalties for late issuance, the certificates themselves remain valid for taxpayers to claim TDS credit.

Conclusion

What is the difference between Form 16 and Form 16A essentially boils down to understanding that Form 16 relates to salary income issued by employers, while Form 16A covers all other income types issued by various deductors. Both serve as crucial TDS certificates helping you file accurate income tax returns and claim appropriate tax credits.

Ensure you receive all applicable forms from your employer and other deductors based on your income sources. Verify the details mentioned in these certificates against your records before using them for ITR filing.

Keep these documents safely for future reference, as they provide essential proof of income earned and taxes paid. Cross-check information in these certificates with your Form 26AS to ensure all TDS is correctly reflected in tax department records.

Understanding income tax forms explained clearly empowers you to handle your tax obligations confidently and avoid common pitfalls. Take time to review these certificates carefully each year, ensuring accuracy and completeness before filing your return.

Frequently Asked Questions

Q1. Can I get both Form 16 and Form 16A from the same person?

No, one entity cannot issue both forms to the same person. Employers issue only Form 16 for salary, while Form 16A covers non-salary payments from any other deductor.

Q2. What if my employer does not provide Form 16?

You can request it from your employer who is legally obligated to issue it. Alternatively, download TDS details from Form 26AS on the Income Tax portal as backup.

Q3. Is Form 16A mandatory for all TDS deductions?

Yes, any deductor who deducts TDS on non-salary payments must issue Form 16A to the deductee within 15 days of filing quarterly TDS returns.

Q4. How can I verify if my Form 16 or Form 16A is genuine?

Cross-check details with your Form 26AS available on the Income Tax e-filing portal. Genuine certificates will match the TDS credit reflected in Form 26AS.

Q5. What should I do if there is a mismatch in Form 16A?

Contact the deductor immediately to issue a revised certificate. If unresolved, report the mismatch while filing ITR and provide supporting documents explaining the discrepancy.

Disclaimer: This article is for informational purposes only. Please verify all information from official government sources before taking action. Procedures and eligibility may vary by state and change over time. We are not responsible for any decisions made based on this content.